Bio-Based Packaging Market Attains USD 34.4 Billion by 2034 | Towards Packaging

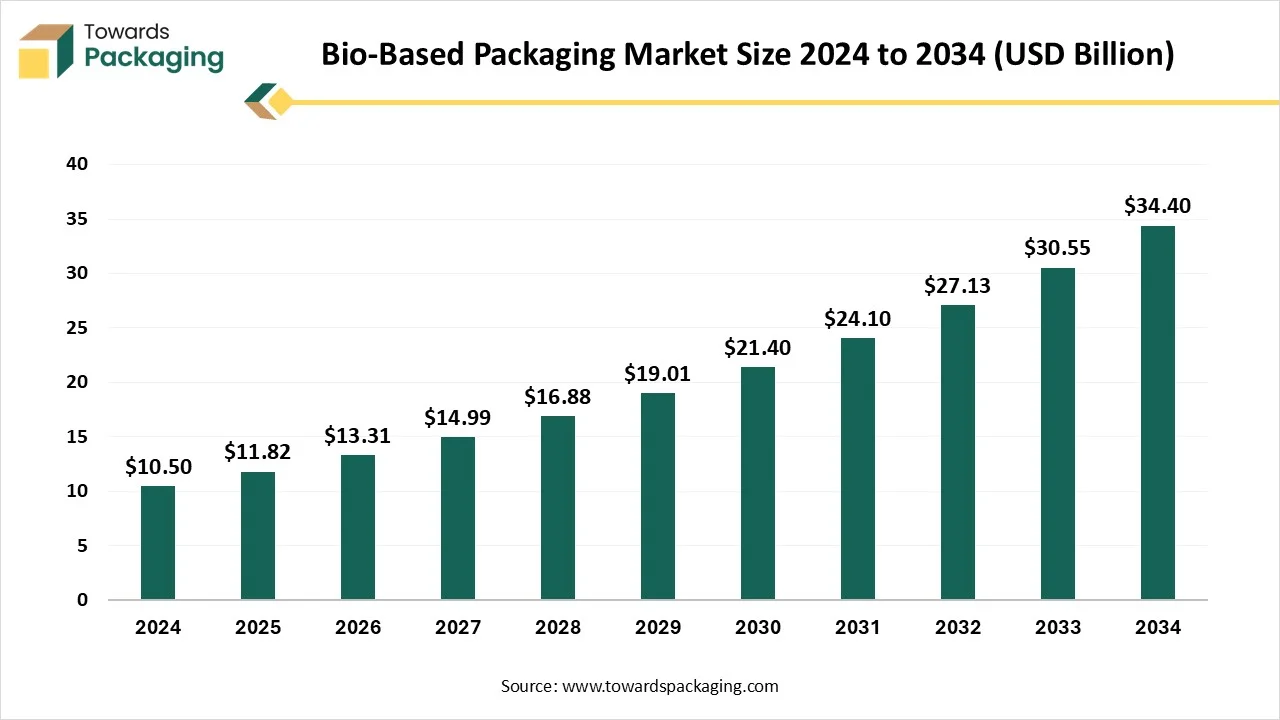

According to Towards Packaging consultants, the global bio-based packaging market is projected to reach approximately USD 34.4 billion by 2034, increasing from USD 10.5 billion in 2024, at a CAGR of 12.60% during the forecast period 2025 to 2034.

Ottawa, Aug. 21, 2025 (GLOBE NEWSWIRE) -- The global bio-based packaging market size stood at USD 11.82 billion in 2025 and is projected to reach USD 34.4 billion by 2034, according to a study published by Towards Packaging, a sister firm of Precedence Research.

The bio-based packaging sector is propelled by mounting environmental concerns, strict regulatory frameworks, and shifting consumer preferences toward sustainable solutions. Companies are innovating with materials like PLA, PHA, algae, seaweed films, mycelium composites, and agricultural waste-based polymers that offer biodegradability, compostability, and reduced carbon emissions ideal for food, beverage, personal care, and healthcare industries.

Get All the Details in Our Solutions – Access Report Sample: https://www.towardspackaging.com/download-sample/5714

Europe leads in adoption, bolstered by regulatory initiatives and strong innovation ecosystems. Yet cost pressures, feedstock shortages, performance limitations, and insufficient recycling or composting infrastructure continue to challenge widespread implementation, underscoring the need for technological advances and improved waste-management systems.

What is Meant by Bio-based Packaging?

Bio-based packaging refers to packaging that are partly or entirely made from renewable biological resources instead of fossil fuels. These biological sources can include plants (like corn, sugarcane, bamboo, hemp), algae, seaweed, mycelium (fungi), or agricultural by products. Unlike conventional plastics derived from petroleum, bio-based packaging uses natural polymers such as polylactic acid (PLA), polyhydroxyalkanoates (PHA), starch blends, or cellulose. Many of these materials are designed to be biodegradable or compostable, reducing environmental impact.

What Are the Key Trends in The Bio-Based Packaging Market?

Innovative, Sustainable Materials:

Researchers are transforming unconventional waste like sewage sludge and eggshells into biodegradable films that boost strength, barrier performance, and even enrich soil with micronutrients upon degradation. Additionally, edible packaging from sustainable sources such as Kodo millet, seaweed, and orange peel is gaining traction.

Regulatory & Circular Economy Drivers:

Laws in the EU (PPWR) and California are pushing for recyclable, reusable, and compostable packaging solutions, spurring the adoption of mono-materials and reusable container systems.

Reusable & Refillable Models:

There's a growing shift toward reusable packaging in sectors like food and beverages. Digital tracking and reusable container pools are becoming more prevalent to support circular practices.

Smart & Active Packaging:

Smart packaging equipped with QR codes, IoT sensors, and NFC enhances transparency and traceability. Emerging bio-based multilayer systems can release active agents like antioxidants or antimicrobials to preserve product freshness. There are even battery-free, stretchable smart packages that autonomously sense and release compounds to prevent spoilage.

Eco-Friendly Barrier Coatings & Inks:

Innovations include natural barrier coatings using starch, cellulose, or waxes, and water-based inks that reduce volatile organic compounds while maintaining performance.

Material Advancements & Scale:

Bioplastics like PLA, PHA, and bio-PET are gaining market share, with production rising rapidly. Asia leads global output, especially in packaging applications. Cutting-edge developments also include bioplastics derived from spirulina or barley starch that are highly biodegradable.

Seaweed, Mycelium & Edible Films:

Bio-based alternatives like seaweed and mushroom-derived films are being embraced for their composability and low environmental footprint. Edible packaging continues to grow in interest as a waste-free option.

If there is anything you'd like to ask, feel free to get in touch with us @ sales@towardspackaging.com

What is the Potential Growth Rate of the Bio-Based Packaging Market?

Environmental Concerns & Climate Goals & Corporate Sustainability Commitments

Rising awareness about plastic pollution, marine litter, and greenhouse gas emissions is pushing governments, industries, and consumers toward eco-friendly alternatives. Bio-based packaging reduces reliance on fossil fuels and helps cut carbon footprints. Bans on single-use plastics, the EU Packaging and Packaging Waste Regulation (PPWR), and U.S. state-level restrictions are accelerating the shift to compostable, recyclable, and renewable packaging materials. Eco-conscious consumers prefer biodegradable or compostable packaging, particularly in food, beverages, cosmetics, and e-commerce sectors. Brand reputation and green labeling also fuel adoption. FMCG giants, retailers, and food chains are pledging to use recyclable or compostable packaging, creating strong demand. Many companies link bio-based packaging with their ESG and circular economy goals.

Limitations & Challenges in the Bio-Based Packaging Market

Regulatory & Certification Barriers and Performance Limitations

The key players operating in the bio-based packaging market are facing issues due to performance limitations and regulatory certification barriers, which are estimated to restrict the market growth. Some bio-based materials lack the durability, heat resistance, or barrier properties required for certain packaging applications, restricting adoption in heavy-duty or long shelf-life products. Many regions lack facilities to properly handle bio-based or compostable packaging, leading to disposal in landfills where biodegradation is slow. This limits real environmental benefits. Confusion between bio-based, biodegradable, and compostable packaging creates mistrust and inconsistent consumer behaviour, slowing widespread acceptance.

More Insights of Towards Packaging:

- Biopharmaceuticals Packaging Market - The biopharmaceuticals packaging market is set to grow from USD 23.01 billion in 2025 to USD 49.98 billion by 2034, at a 9% CAGR.

- Bioplastic Packaging Market - The global bioplastic packaging market size is forecast to grow from US$ 21.08 billion in 2024 to hit US$ 103.09 billion by 2034, expanding at a CAGR of 17.2%.

- Biotechnology Labels and Packaging Market - The global biotechnology labels and packaging market is undergoing rapid expansion, with revenue projections reaching hundreds of millions between 2025.

- Biologics CDMO Secondary Packaging Market - The biologics CDMO secondary packaging market is projected to reach USD 5.50 billion by 2034, expanding from USD 2.59 billion in 2025.

- Biodegradable Plastic Films Market - The biodegradable plastic films market is predicted to expand from USD 1.31 billion in 2025 to USD 1.95 billion by 2034, growing at a CAGR of 4.50%.

- Biohazard Bags Market - The biohazard bags market is projected to reach USD 1046.68 million by 2034, expanding from USD 536.15 million in 2025, at an annual growth rate of 7.60%.

- Biodegradable Paper and Plastic Packaging Market - The global biodegradable paper and plastic packaging market size reached US$ 15.43 billion in 2024 and is projected to hit around US$ 40.75 billion by 2034.

- Biobased Films Market - The bio-based films market is forecasted to expand from USD 4.92 billion in 2025 to USD 12.59 billion by 2034, growing at a CAGR of 11.5% from 2025 to 2034.

- Starch-based Bioplastics Market - The global starch-based bioplastics market size was evaluated at US$ 1.94 billion in 2024 and is expected to attain around US$ 5.26 billion by 2034.

- Bioengineered Packaging Market - The bioengineered packaging market is expected to increase from USD 581.67 billion in 2025 to USD 1000.64 billion by 2034, growing at a CAGR of 6.24%.

-

Cell Culture Media Storage Containers Market - The global cell culture media storage containers market is anticipated to grow from USD 2.42 billion in 2025 to USD 7.04 billion by 2034.

Regional Analysis:

Who is the Leader in the Bio-Based Packaging Market?

The Asia-Pacific region dominates the bio-based packaging market due to its strong manufacturing base, abundant availability of agricultural feed stocks such as corn, sugarcane, and starch, and rapidly growing consumer demand for sustainable alternatives. Rising urbanization, e-commerce growth, and increasing awareness of plastic pollution are further driving adoption across the food, beverage, and personal care sectors. Governments in countries like China, Japan, and India are implementing stricter plastic bans and offering incentives for eco-friendly packaging solutions.

China Market Trends

China leads the region, driven by explosive e-commerce growth, especially in Tier 1–2 cities, with parcel volumes reaching nearly 175 billion units in 2024. This surge fuels demand for sustainable, high-performance packaging solutions like fiber-based formats and smart-trackable cartons. Government mandates such as the 2024 Express Packaging Standard GB 43352 and updated delivery regulations pressure couriers and brands toward recyclable and biodegradable materials. In construction, urbanization also spurs bio-composites demand for eco-friendly building materials, indirectly boosting broader bio-based material adoption.

India Market Trends

India is the fastest-growing market in the region, propelled by its massive agricultural base, rising R&D in packaging materials, increasing bio-based consumer awareness, and thriving e-commerce and food sectors. For example, SIG is investing ₹360 crore to expand packaging production, with plans to scale output from 4 to 10 billion packs annually. The agricultural packaging market also favors biodegradable and jute-based materials, supported by mainstream shifts toward sustainability.

Japan Market Trends

Japan is making notable progress through technological innovation in biobased materials. In October 2024, Teijin Frontier launched its BIOFRONT polylactic acid (PLA) resin, offering faster biodegradation in natural environments while retaining material integrity. Mitsubishi Chemical Group developed BioPBS, a compostable bio-based polymer used in teabag pouches, combining flexibility and low-temperature sealing for food packaging.

South Korea Market Trends

South Korea is increasingly adopting biocomposites in sectors like automotive for lightweighting, a key strategy for improving fuel efficiency and meeting environmental targets. Biocomposites are replacing heavier materials in interiors and trim, especially as the shift to electric vehicles intensifies. Additionally, South Korean firms are showcasing recyclable copolyesters such as ECOTRIA CLARO at international beauty expos, blending luxury aesthetics with PET-stream recyclability.

How is the Opportunistic Rise of Europe in the Bio-Based Packaging Market?

Europe is experiencing rapid growth in the bio-based packaging market, driven by stringent environmental regulations, strong consumer demand for sustainable products, and significant investments in bioplastics innovation. The European Union's Single-Use Plastics Directive and the European Green Deal have mandated reductions in plastic waste, compelling industries to adopt biodegradable and recyclable alternatives. In 2024, packaging remained the largest segment for bioplastics, accounting for 45% of the total market.

Countries like Germany, France, and Italy are leading in bioplastics production and consumption, supported by well-established recycling infrastructures and a culture of sustainability. Recent developments include the launch of compostable packaging solutions by major FMCG brands and the expansion of bioplastics production capacities to meet growing demand. These factors collectively position Europe as a leader in the global bio-based packaging market.

Germany Market Trends

Germany leads Europe's biobased packaging sector with advanced engineering, robust recycling infrastructure, and stringent circular economy policies like the Packaging Act (VerpackG) and EU-aligned Waste Prevention Program 2023. Industry giants such as BASF and Südpack are innovating with PHA, PLA, and paper–laminate biodegradable solutions, especially across food service, e-commerce, and cosmetics. In August 2024, Alpla’s collaboration with startup Sea Me launched zerooo reusable PET bottles with a deposit-return system, boosting circularity in cosmetic packaging.

France Market Trends

France’s aggressive regulatory environment, driven by the AGEC Anti-Waste Law, bans single-use plastics and pushes for eco-design, strengthening the market for compostable films, molded pulp trays, and seaweed-based packaging. The government and EU offer subsidies to startups and SMEs to accelerate bio-based packaging adoption in the retail and hospitality sectors.

Italy Market Trends

Italy is harnessing its agricultural sector to convert agro-waste, like winery, olive oil, and tomato byproducts, into biodegradable packaging. EU initiatives like Horizon Europe support pilot programs in this bio-economy transformation. A notable move in late 2024 saw French Sphere Group acquire Romagnasac (known for Virosac and Rapid), expanding bio-based flexible packaging capacity in Italy and enhancing cross-border collaboration.

How Big is the Success of the North American Bio-Based Packaging Market?

North America’s bio-based packaging sector benefits from a strong and evolving regulatory environment, with states like California, New York, and Washington enforcing Extended Producer Responsibility (EPR) programs and single-use plastic bans, which elevate demand for compostable alternatives. Government incentives, including grants to expand composting infrastructure (USD 75 million) and advanced packaging programs, are accelerating material innovation and adoption. Growing consumer demand for sustainable products, especially in food, healthcare, and e-commerce, also fuels uptake. Finally, advances in material science, such as improved PLA, PHA, and PBS formulations, enhance performance, cost competitiveness, and scalability across diverse applications.

U.S. Market Trends

The U.S. market is accelerating on the back of fast-spreading packaging EPR laws (California SB 54 already in implementation; more states adding EPR in 2025), which push producers toward reusable, recyclable, and compostable formats and fund end-of-life systems. Federal and state recycling/composting infrastructure grants (e.g., EPA’s SWIFR awards) are upgrading organics and recycling capacity, improving the business case for PLA, PHA, paper/fiber, and coated-cellulose solutions. Industry capacity is also expanding: analysts expect the highest global growth in bio-based polymer capacity in North America through 2029, notably in PHA.

Canada Market Trends

Canada’s Single-Use Plastics Prohibition Regulations (SUPPR) covering items like checkout bags, cutlery, and certain foodservice ware continue to steer brands toward fiber, molded-pulp, and certified-compostable formats. While a 2023 court ruling challenged the federal listing underpinning the ban, the federal appeal and stay have kept the national prohibitions in force, sustaining industry momentum as provinces and municipalities advance complementary waste and organics programs. The policy signal, combined with retailer commitments and municipal organics expansion, is supporting demand for bio-based alternatives and packaging redesign.

How Crucial is the Role of Latin America in the Bio-Based Packaging Market?

Latin America is growing at a considerable rate in the bio-based packaging market due to supportive regulatory frameworks, rising sustainability awareness, and strong agricultural resources that serve as feedstocks for bioplastics. Countries like Brazil, Mexico, and Chile are implementing plastic reduction laws and bans on single-use plastics, encouraging industries to adopt bio-based and compostable alternatives.

The region’s large food and beverage sector, coupled with growing e-commerce and retail packaging needs, is fueling demand for sustainable solutions. Additionally, global brand owners operating in Latin America are committing to eco-friendly packaging goals, driving regional investments. A recent example is Brazil’s initiatives promoting sugarcane-based bioplastics, which are increasingly being integrated into food packaging and consumer goods.

How will the Middle East and Africa Grow in the Bio-Based Packaging Market?

The Middle East and Africa region presents a significant opportunity for growth in the bio-based packaging market, driven by rising environmental awareness, rapid urbanization, and increasing demand for sustainable packaging in the food, beverage, and FMCG sectors. Governments in countries such as Saudi Arabia, the UAE, and South Africa are introducing strict bans on single-use plastics and promoting alternatives, creating strong regulatory support for bio-based solutions. The region’s agricultural resources also enable the production of bioplastics like PLA and PHA. Recent developments, including sugarcane-based bioplastics in South Africa and eco-friendly initiatives in the GCC, highlight accelerating adoption, positioning MEA as an emerging hub for sustainable packaging solutions in the coming decade.

Join now to access the latest packaging in industry segmentation insights with our Annual Membership: https://www.towardspackaging.com/get-an-annual-membership

Segment Outlook

Material Type Insights

The bioplastic segment dominates the market due to its versatility, scalability, and wide application across industries such as food and beverages, personal care, and e-commerce. Bioplastics, including PLA, PHA, and starch blends, are increasingly favored because they combine performance properties similar to conventional plastics with reduced environmental impact. Rising consumer demand for eco-friendly packaging, along with government regulations restricting single-use plastics, further boosts adoption.

Additionally, technological advancements and investments in bioplastic production have lowered costs and improved durability, transparency, and heat resistance, making them suitable for diverse packaging needs.

The polyhydroxyalkanoate (PHA) segment is the fastest-growing material type in the bio-based packaging market due to its fully biodegradable and compostable properties, even in marine and soil environments, making it a sustainable alternative to conventional plastics. PHAs are produced from renewable feedstocks through microbial fermentation, aligning with circular economy goals and reducing reliance on fossil fuels. Increasing regulatory restrictions on single-use plastics and growing consumer preference for eco-friendly packaging accelerate demand.

Moreover, technological advancements and investments in large-scale PHA production have improved cost efficiency and performance, enabling applications in food packaging, agriculture, and medical products, driving rapid market expansion.

Packaging Format Insights

The flexible packaging segment dominates the market because of its lightweight, cost-effective, and versatile nature, which reduces material usage and transportation costs compared to rigid alternatives. It is widely adopted in food, beverage, and personal care industries due to its ability to extend shelf life, maintain product freshness, and offer convenient formats such as pouches, sachets, and wraps. Growing demand from e-commerce and retail also supports its expansion. Furthermore, innovations in bioplastics like PLA and starch blends have improved barrier properties, making flexible biobased packaging a sustainable yet functional solution, thereby reinforcing its dominance in the global market.

The rigid packaging segment is the fastest-growing format in the bio-based packaging market due to its durability, strength, and ability to protect products from damage and contamination, making it highly suitable for food, beverages, cosmetics, and healthcare products. Rising consumer demand for sustainable alternatives to conventional rigid plastics has accelerated the adoption of biobased materials such as PLA, PHA, and bio-PET in bottles, jars, and containers. Additionally, increasing government regulations on single-use plastics and brand owners’ commitments to circular economy goals are driving innovation in rigid biobased packaging.

Application Insights

The primary packaging segment dominates the market because it directly encases and protects products, ensuring safety, freshness, and extended shelf life—crucial for industries like food, beverages, pharmaceuticals, and personal care. Increasing consumer preference for eco-friendly packaging has pushed brands to adopt biobased materials for bottles, pouches, films, and blister packs. Moreover, strict regulations on conventional plastics in primary packaging, especially for food-contact applications, are boosting demand. Bioplastics such as PLA and bio-PET provide the necessary barrier properties and durability while reducing environmental impact.

The secondary packaging segment is the fastest-growing application segment in the market due to rising demand from e-commerce, retail, and logistics sectors, where packaging is essential for product grouping, protection, and branding. Companies are increasingly shifting toward sustainable solutions for cartons, boxes, and wraps made from biobased materials to meet corporate sustainability goals and comply with environmental regulations.

Additionally, consumer preference for eco-friendly outer packaging is influencing brands to adopt greener alternatives. Recent innovations in biobased films, molded fiber, and coatings are enhancing strength and printability, making secondary packaging both functional and sustainable, thereby driving its rapid market growth.

End-Use Industry Insights

The food and beverage segment dominates the bio-based packaging market because of its high consumption volume and strict demand for sustainable, safe, and functional packaging solutions. Bio-based packaging materials such as PLA, bio-PET, and starch blends are widely used in bottles, pouches, films, trays, and containers to preserve freshness, extend shelf life, and ensure food safety. Rising consumer awareness of eco-friendly alternatives and increasing regulations on single-use plastics in food packaging further accelerate adoption.

Major food and beverage companies are also committing to sustainability goals, investing in biodegradable and compostable packaging, which reinforces this segment’s leadership in the global bio-based packaging market.

The healthcare and pharmaceuticals segment is the fastest-growing industry segment in the market due to the increasing demand for safe, sterile, and sustainable packaging solutions. Biobased materials such as PLA, PHA, and bio-PET are being adopted for blister packs, bottles, vials, and pouches that require durability, barrier protection, and compliance with stringent regulatory standards.

Growing environmental concerns and regulations to reduce plastic waste are pushing pharmaceutical companies to integrate eco-friendly alternatives. Additionally, rising investments in sustainable healthcare supply chains and innovation in biodegradable medical packaging materials are accelerating growth, making this segment one of the most dynamic in the market.

Elevate your packaging strategy with Towards Packaging. Enhance efficiency and achieve superior results - schedule a call today: https://www.towardspackaging.com/schedule-meeting

Recent Breakthroughs in the Global Market:

- In March 2025, LyondellBasell, a company focused on manufacturing chemicals, revealed the introduction of Pro-fax EP649U, a novel polypropylene impact copolymer intended for the rigid packaging market. Food packaging applications benefit greatly from this novel product, which is especially designed for thin-walled injection molding. Fast crystallization and high flow characteristics of the Pro-fax EP649U allow for the effectively producing thin-walled containers while increasing output and quality of the product.

- In August 2025, Cortec, a company developing corrosion solutions for industries, revealed the introduction of the Eco Works 100 packaging film, which is certified as industrially compostable by TUV Austria and is claimed to contain 100% USDA-certified biobased content.

Access our exclusive, data-rich dashboard dedicated to the bio-based packaging market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is your one-stop gateway to actionable insights.

Access Now: https://www.towardspackaging.com/contact-us

Bio-Based Packaging Market Players

- NatureWorks LLC

- BASF SE

- Novamont S.p.A.

- TotalEnergies Corbion PLA

- Braskem S.A.

- Stora Enso Oyj

- Huhtamaki Oyj

- Amcor Plc

- Tetra Pak International S.A.

- Mondi Group

- International Paper

- Smurfit Kappa Group Plc

- Sonoco Products Company

- Innovia Films (now part of CCL Industries)

- TIPA Corp. Ltd.

- Futamura Chemical Co., Ltd.

- Danimer Scientific

- Biome Bioplastics Limited

- PTT Global Chemical Public Company Limited (PTT GC)

- Alpla Group

Bio-Based Packaging Market Segments

By Material Type

-

Bioplastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Starch Blends

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Polybutylene Adipate Terephthalate (PBAT)

- Other Biodegradable Bioplastics

- Other Bio-based Non-Biodegradable Plastics

- Paper & Paperboard (from sustainable sources)

- Wood Fiber-Based Materials

- Other Natural Fibers (e.g., bamboo, sugarcane bagasse, mushroom mycelium, seaweed)

By Packaging Format

-

Rigid Packaging

- Bottles & Jars

- Trays & Containers

- Clamshells

-

Flexible Packaging

- Pouches & Sachets

- Bags & Wraps

- Films

By Application

- Primary Packaging

- Secondary Packaging

- Tertiary/Transport Packaging

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Consumer Electronics

- E-commerce & Retail

- Other Consumer Goods

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Invest in Our Premium Strategic Solution: https://www.towardspackaging.com/price/5714

Become a Valued Research Partner with Us - Schedule a meeting: https://www.towardspackaging.com/schedule-meeting

Request a Custom Case Study Built Around Your Goals: sales@towardspackaging.com

About Us

Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry.

Stay Connected with Towards Packaging:

- Find us on Social Platforms: LinkedIn | Twitter | Instagram

- Subscribe to Our Newsletter: Towards Sustainable Packaging

- Visit Towards Packaging for In-depth Market Insights: Towards Packaging

- Read Our Printed Chronicle: Packaging Web Wire

-

Get ahead of the trends – follow us for exclusive insights and industry updates:

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire - Contact: APAC: +91 9356 9282 04 | Europe: +44 778 256 0738 | North America: +1 8044 4193 44

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.